New Markets Tax Credits

This program was established to incentivize the use of the NMTC program in the State’s underserved and underdeveloped areas. These are identified by the federal government as having unemployment greater than 1.5 times the national average and those areas with median incomes less than 80% of the state or metropolitan area.

AIDEA envisions this program to be a partnership with Alaska’s financial institutions by sharing in the risk that is inherent to these transactions. The sharing of risk will encourage more NMTC transactions to be considered in these areas with the resulting economic development having a significant impact on the local community and economy.

For more information on NMTC and eligibility please see Federal New Markets Tax Credit Program below.

The NMTC transaction generally has two distinct pieces: 1/ Equity, gained from the sale of NMTC, and 2/ debt gained from leveraging the equity contribution. AIDEA’s program is specifically focused on the Leveraged Loan portion of the transaction as this is often the most difficult to secure.

NMTC transactions can be used to finance a large range of business types including commercial, retail, industrial, mixed-use, and community facilities. NMTCs are excluded from financing residential rental housing if more than 80% of the gross income is generated from the residential portion of the development. Ineligible activities include: golf courses and country clubs, gambling facilities, liquor stores, some farming businesses, massage parlors, tanning salons and spas.

Investments in or loans to operating businesses can be used for a variety of reasons including: plant expansion, capital equipment purchases (equipment, parts, inventory, or FF&E), and short term working capital.

Application Process

AIDEA’s program has two components:

1. Loan Guarantee, and

2. Direct Loan

Loan Guarantee

The applicant must have been awarded a NMTC allocation from a Community Development Entity, or be in the process of securing that allocation from one or more CDE’s. The applicant may then apply to AIDEA for a guarantee of the leveraged loan portion of the NMTC transaction. If, and when, AIDEA issues a Letter of Commitment the applicant can use it to secure a commercial loan to the transaction from an eligible financial institution. If a loan is secured, AIDEA will work with the lender to ensure the terms and conditions of the guarantee and the loan are compatible and acceptable to both parties. The guarantee will be executed at the closing of the NMTC transaction.

Direct Loan

AIDEA may make a loan under this program only if it determines that the applicant was unable to use AIDEA’s Letter of Commitment to obtain a loan from a financial institution under commercially reasonable terms. In this case the applicant will be required to submit documentation demonstrating that at least two financial institutions have reviewed and rejected a loan application or that the application was approved but subject to terms AIDEA determines are commercially unreasonable.

The application will undergo a comprehensive underwriting process in which AIDEA will determine:

· if the borrower is creditworthy

· the financially and economically feasibility of the business plan

· the viability of any collateral

· the projected revenues are sufficient to cover operations, maintenance and debt service

· if there is any other information required to determine the strength of the project.

For more information regarding the New Markets Tax Credit Assistance Guarantee and Loan Program, contact AIDEA 907-771-3000.

Federal New Markets Tax Credit Program

In December 2000, Congress enacted the New Markets Tax Credit Program (NMTC) as part of the Community Renewal Tax Relief Act of that same year. The New Markets program is designed to encourage investments in low-income communities that traditionally have had poor access to debt and equity capital.

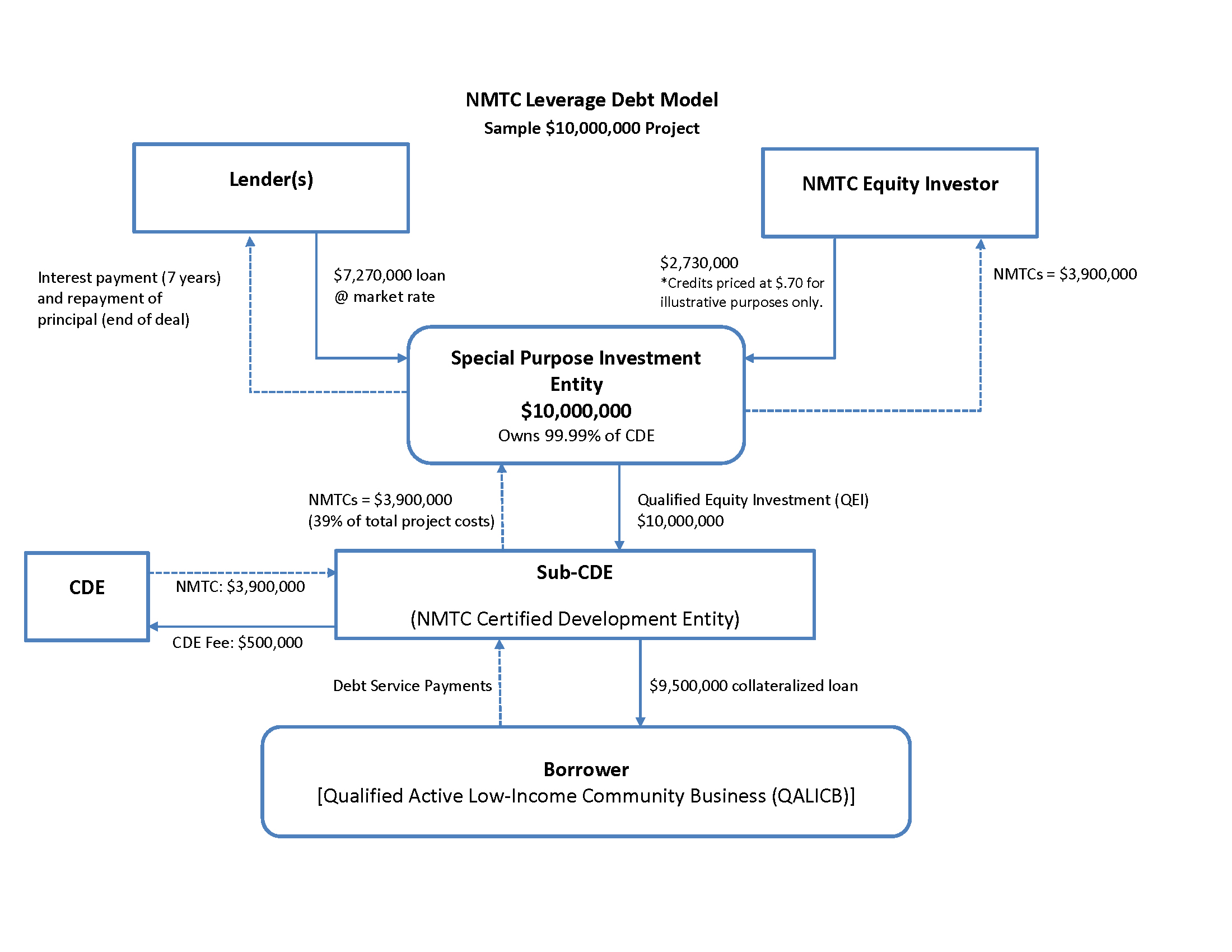

The NMTC program provides a credit against federal income taxes of 39% over 7 years to taxpayers who make Qualified Equity Investments (QEIs) in a Community Development Entity (CDE). CDEs use the capital from investors to provide financing to businesses located in low income communities. Examples of a CDE are a community development corporation, a community loan fund, a regulated financial institution, and a state or local government entity.

CDEs compete for annual allocations of New Markets Tax Credits. CDEs write applications that discuss their strategy to make investments using NMTC that achieve significant community impacts, and that describe their management capacity and ability to raise capital. Upon receiving an allocation, CDEs market the Credit to taxpayers who receive the 39% credit for their investment over 7 years. With those funds CDEs make loans or equity investments in businesses in low income communities. Except for rental housing, NMTCs can be used to subsidize almost any type of business or real estate project, including community facilities and other nonprofit uses such as schools, health clinics and cultural institutions. These businesses are defined under the law as Qualified Active Low Income Community Businesses (QALICBs) and include real estate projects or operating or start-up businesses.

NMTCs can be used to leverage the equity investment with regular loans from financial institutions or other sources. These are made as nonrecourse loans and are interest only for seven years.

Only projects in Qualified Census Tracts (QCT) are eligible for the NMTC tax credits. QCTs are those that meet at least one of the following requirements:

- Poverty rate greater than 20%; or

- Median income less than 80% of the state/metropolitan median; or

- Targeted populations

- Population is less than 2000 people, contiguous to a Low Income Community (LIC) and in an empowerment zone, or

- High migration rural counties (85% median income)

To see if your project site is in a QCT, click on the following link: https://www.novoco.com/new_markets/resources/maps_data.php

Qualified Businesses

Any corporation or partnership (including nonprofits) engaged in the active conduct of a qualified business that meets all 5 requirements:

- Gross Income (50% LIC)

- Tangible Property (40% LIC)

- Services Performed (40% LIC)

- Collectibles (< 5% property)

- Nonqualified Financial Property (< 5% property)

Ineligible Activities

- Residential rental property:

- Buildings which derive 80% or more of income from residential dwelling units

- Certain types of businesses:

- Businesses primarily - Farming businesses with having intangibles assets over $500,000 for sale/license - Stores where the principal business is the sale of alcoholic beverages

- Golf courses

- Race tracks

- Gambling facilities

The benefits to the borrower may include:

- Lower cost of borrowing

- 25% reduced cost

- Lower interest rate

- Debt forgiveness

- Favorable terms may include:

- 7 years interest only

- Higher Loan To Value ratio

- Lower collateral

New Markets Tax Credit Model